Navigating the Digital Frontier: Digital Banking vs. Fintech Apps Explained

A Comprehensive Guide to Understanding the Modern Financial Landscape and Your Choices

The world of money is changing faster than ever, with new digital platforms promising convenience at every turn. But are you truly aware of the fundamental differences shaping your financial future?

From managing daily expenses to investing in the markets, a proliferation of apps and services now compete for your attention. How do you choose the right digital partner for your unique financial needs?

Beyond flashy interfaces, the core mechanics of how your money is handled vary wildly across the digital spectrum. Understanding these distinctions is no longer optional; it’s essential for modern financial empowerment.

The financial services industry has undergone a monumental transformation in recent decades, moving far beyond the traditional brick-and-mortar bank branch. The advent of the internet and, more profoundly, the ubiquitous smartphone, has ushered in an era of digital-first financial interactions. Today, consumers are faced with a dizzying array of options, from established banks offering advanced online services to nimble startups providing specialized financial tools. This rapid evolution often leads to confusion, particularly when trying to differentiate between Digital Banking vs Fintech Apps.

While both aim to simplify and enhance financial management through technology, they operate on distinct models, adhere to different regulatory frameworks, and offer varying scopes of services. Understanding these nuances is crucial for making informed decisions about where to entrust your money and how to manage your financial life effectively. This comprehensive guide will examine the characteristics of traditional banking, digital banking, and fintech applications, providing a clear breakdown of their definitions, advantages, disadvantages, and key distinctions, ultimately empowering you to navigate this dynamic digital financial frontier with confidence.

Quick navigation

- The Evolving Landscape of Financial Services: A Digital Revolution

- Defining the Players: Traditional Banking, Digital Banking, and Fintech Apps

- Digital Banking: The Full-Service Online Experience

- Fintech Apps: Specialized Innovation at Your Fingertips

- Key Distinctions: Where Do They Diverge?

- What this means for you

- Risks, trade-offs, and blind spots

- Main points

The Evolving Landscape of Financial Services: A Digital Revolution

For centuries, financial services were synonymous with physical institutions: ornate bank branches, stern-faced tellers, and mountains of paperwork. Trust was built on tangibility, on the reassuring presence of a physical edifice. However, the dawn of the internet age began to chip away at this model, offering the first glimpses of online banking. This initial digital foray was often clunky, a mere digital replication of existing paper processes. It wasn't until the widespread adoption of smartphones and the explosion of mobile applications that the financial sector truly began its digital revolution.

Today, consumer expectations have fundamentally shifted. We demand instant access, seamless transactions, personalized insights, and the ability to manage our money from anywhere, at any time. This demand has not only forced traditional banks to radically overhaul their digital offerings but has also paved the way for an entirely new breed of financial providers. These new players, unburdened by legacy infrastructure, have been able to build services from the ground up with digital convenience at their core. The result is a vibrant, competitive, and sometimes confusing ecosystem where different models of financial service coexist. Has the traditional bank branch become an artifact of a bygone era, or does it still hold unique value?

This evolving landscape offers unprecedented choice and innovation, but also necessitates a clearer understanding of the various entities operating within it. Without this clarity, consumers risk misplacing trust, overlooking critical features, or failing to utilize the best tools for their specific financial needs. The distinction between a bank that is digital-first and a technology company offering financial services is more than just semantics; it carries significant implications for security, scope, and the very nature of your financial relationship.

Defining the Players: Traditional Banking, Digital Banking, and Fintech Apps

To truly understand the modern financial world, we must first establish clear definitions for its primary players. While they all deal with money, their operational structures, regulatory oversight, and service models can differ significantly.

Traditional Banking: These are the familiar institutions that have been around for decades, if not centuries. They operate with a full banking license, allowing them to accept deposits, issue loans, and offer a wide array of financial products. Their defining characteristic has historically been a physical branch network, providing in-person customer service and a tangible sense of security. While they have significantly expanded their digital presence with online and mobile banking, these digital channels often function as an extension of their existing, often complex, legacy systems.

- Pros: Established trust and reputation, extensive product range (mortgages, complex investments), personalized in-person service, robust regulatory oversight and deposit insurance (e.g., FDIC in the US).

- Cons: Slower to innovate, often higher fees (account maintenance, overdrafts), less agile digital interfaces, sometimes outdated technology, limited operating hours for branches.

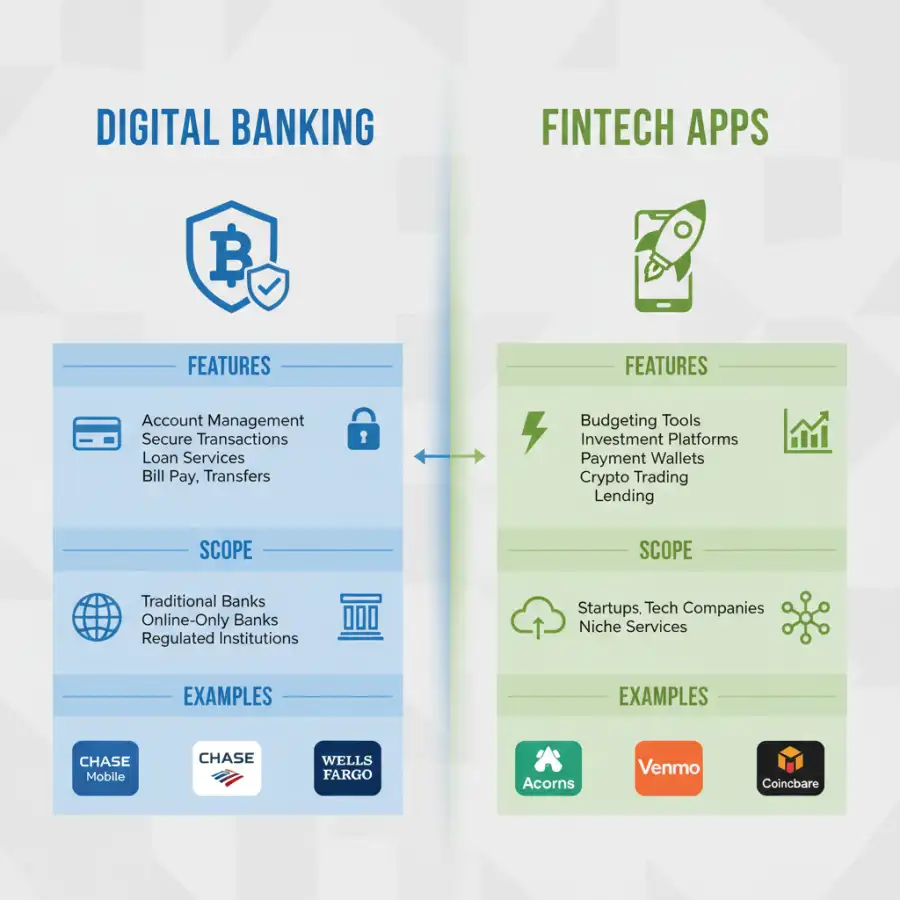

Digital Banking (Neobanks/Challenger Banks): These are fully online banks with no physical branches. They conduct all their operations through mobile apps and websites. Digital banks either possess their own full banking license or, more commonly, partner with an existing licensed bank to offer insured financial products. Their core appeal lies in utilizing modern technology to offer streamlined services, lower fees, and superior user experiences, often targeting tech-savvy consumers and those underserved by traditional institutions.

- Pros: Low or no fees, high-interest savings accounts, advanced mobile features (budgeting tools, real-time alerts), rapid account setup, excellent user experience (UX), 24/7 digital access.

- Cons: Lack of physical presence (can be an issue for cash deposits/withdrawals, complex inquiries), potentially fewer complex financial products (e.g., specialized loans, wealth management), reliance on digital customer service.

Fintech Apps (Financial Technology Applications): This is a broad category encompassing technology-driven companies that offer specific financial services. Unlike digital banks, fintech apps are not necessarily licensed banks themselves. They often focus on a single aspect of finance, such as budgeting, investing, payments, or lending, and frequently partner with traditional banks to hold user funds or process transactions. Examples include popular budgeting tools, stock trading apps, peer-to-peer payment platforms, or micro-lending services.

- Pros: Hyper-specialized features, pioneering innovation, superior user experience for their specific niche, personalized insights, quick adoption of new technologies.

- Cons: Services can be fragmented (requiring multiple apps for full financial management), varied regulatory oversight (may not offer deposit insurance directly), potential for less comprehensive customer support, risk of data privacy concerns due to extensive data collection.

Are these just different shades of the same service, or are we witnessing fundamentally distinct approaches to managing money?

Digital Banking: The Full-Service Online Experience

Digital banks, often referred to as neobanks or challenger banks, represent a significant paradigm shift from traditional banking. Their defining characteristic is the complete absence of physical branches, with all services delivered exclusively through intuitive mobile applications and web platforms. This branchless model is not merely a cost-cutting measure; it's a fundamental aspect of their operational efficiency and customer value proposition. By eliminating the immense overheads associated with maintaining a physical footprint, digital banks can pass on significant savings to their customers in the form of lower fees, higher interest rates on deposits, and more favorable exchange rates for international transactions.

The core offerings of digital banks are comprehensive, mirroring those of traditional institutions: checking accounts, savings accounts, debit cards, mobile payment services, and often personal loans or credit lines. What sets them apart is the seamless, real-time digital experience. Users benefit from instant transaction notifications, advanced budgeting tools integrated directly into the app, easy categorization of spending, and features like round-ups for savings. Account setup is typically quick and entirely paperless, often completed in minutes directly from a smartphone. These institutions are designed with a mobile-first philosophy, making financial management feel less like a chore and more like an integrated part of daily digital life. This focus on user experience and efficiency positions them at the forefront of top fintech trends.

Crucially, digital banks operate under robust regulatory frameworks. Many are fully licensed banks themselves (e.g., N26 in Europe, Monzo in the UK), while others partner with established, insured banks to provide their services (e.g., Chime in the US). This means that customer deposits are typically insured up to the standard limits (e.g., FDIC in the US), providing a level of security and trust comparable to traditional banks. Their appeal is particularly strong among younger, tech-savvy demographics who prioritize convenience and value innovative digital features over the need for in-person interactions. Could a digital-only bank truly replace every aspect of your traditional financial life?

Fintech Apps: Specialized Innovation at Your Fingertips

Fintech apps occupy a unique and diverse space within the digital financial ecosystem. Unlike digital banks that aim to provide a comprehensive banking experience, most fintech apps are designed to solve a very specific financial pain point or enhance a particular aspect of money management. They are characterized by their specialization, agile development, and often a superior, highly focused user experience for their niche function.

Consider the breadth of services offered by fintech apps:

- Budgeting and Expense Tracking: Apps like Mint or YNAB (You Need A Budget) connect to your existing bank accounts, aggregating financial data and providing detailed insights into spending patterns, helping users stick to financial goals.

- Investment and Trading: Platforms like Robinhood and Acorns democratized investing, offering commission-free trades or micro-investing capabilities that were once exclusive to traditional brokerages. Wealthfront, meanwhile, pioneered automated investment advice.

- Payment Services: PayPal, Venmo, and Square Cash (Cash App) transformed peer-to-peer payments, making it effortless to send and receive money, often instantly, between individuals or for small business transactions.

- Lending: Fintech lenders such as Kabbage (for small businesses) or LendingClub (for personal loans) use alternative data and faster algorithms to provide quicker loan approvals and often more tailored rates than traditional banks.

The primary value proposition of these apps is their ability to deliver a highly focused, often advanced solution to a specific financial need. They utilize advanced algorithms, artificial intelligence, and sophisticated data analytics to offer personalized insights, automate financial tasks, and create incredibly user-friendly interfaces for their chosen domain. The regulatory landscape for fintech apps is much more varied than for banks. Some might be regulated as money transmitters, others as investment advisors, and some operate with less direct oversight, often relying on partnerships with licensed banks for core financial functions. This regulatory diversity is a key distinction. Their specialized nature makes them ideal for consumers and small businesses embracing digital solutions to tackle particular financial challenges. Is it possible for a collection of specialized apps to provide a more holistic financial experience than a single, comprehensive bank?

Key Distinctions: Where Do They Diverge?

While all players in the modern financial ecosystem strive to serve your monetary needs, their fundamental differences lie in several key areas. Understanding these divergences is essential for consumers to make informed choices that align with their personal priorities and financial comfort levels.

- Regulatory Framework & Trust: This is arguably the most critical distinction. Digital banks typically operate with a full banking license or partner with a licensed institution, meaning they offer deposit insurance (like FDIC or FSCS protection). This provides a robust safety net for your funds. Fintech apps, on the other hand, have a more varied regulatory landscape. Some are regulated under specific financial licenses (e.g., money transmission licenses), while others might operate primarily as technology companies. While many are secure, they may not offer the same direct deposit insurance as a fully licensed bank, impacting the perceived level of consumer protection and trust.

- Scope of Services: Digital banks aim to be comprehensive, providing all essential banking services under one roof – checking, savings, debit cards, loans, and payment facilities. Their goal is to replace your primary bank. Fintech apps are generally specialized. You might use one for budgeting, another for investing, and yet another for peer-to-peer payments. This specialization can lead to superior features for a particular task but requires users to manage multiple platforms for a complete financial picture.

- Physical Presence: Traditional banks maintain physical branches, offering in-person service, which can be invaluable for complex issues, cash handling, or simply for those who prefer face-to-face interaction. Both digital banks and fintech apps are purely digital, relying on online and mobile channels for all interactions. This can be a boon for convenience but a drawback for those who value personal touch or need physical access to services.

- Business Model: Digital banks typically thrive on lower operational overheads, passing savings to customers through reduced fees or higher interest rates. Their revenue comes from interchange fees on card transactions and interest on loans. Fintech apps' business models are diverse, ranging from transaction fees, subscription models for premium features, interest on invested funds, or even data monetization.

- Customer Support: Traditional banks offer a mix of in-person, phone, and digital support. Digital banks primarily rely on in-app chat, email, and phone support, often available 24/7 but without a physical location to visit. Fintech apps' customer support can vary widely in quality and availability, depending on the company's size and resources.

When is a digital-first approach a distinct advantage, and when does it become a critical limitation for users?

What this means for you

In this rapidly evolving financial ecosystem, the distinctions between traditional banks, digital banks, and fintech apps have significant implications for how you manage your money. Your choice should ideally align with your personal financial habits, priorities, and comfort level with digital interactions. The power of choice now rests firmly in your hands, allowing you to tailor your financial tools to your unique lifestyle.

If you prioritize convenience, low fees, advanced budgeting tools, and a seamless mobile experience, a digital bank might be an excellent primary banking solution. They are particularly well-suited for individuals comfortable with entirely virtual interactions and who rarely need in-person services. For those with specific financial pain points, such as detailed expense tracking, micro-investing, or specific lending needs, specialized fintech apps can provide unparalleled functionality and a superior user experience in their niche. These apps often complement a primary banking relationship, whether with a traditional or digital bank, rather than replacing it entirely.

For individuals who value the security of in-person service, require complex financial advice (e.g., mortgages, estate planning), or simply prefer the tangible reassurance of a physical branch, traditional banking still holds considerable value. However, even traditional banks have been forced to innovate, increasingly offering robust digital tools to compete. This has led to the rise of hybrid models, where traditional banks enhance their digital offerings, and fintech apps increasingly partner with licensed banks to provide greater security and regulatory compliance. This increased competition and innovation ultimately benefit you, the consumer, offering more choices and better services across the board. For an ultimate guide to FinTech, understanding this diverse landscape is crucial. In this diverse financial landscape, how do you tailor your choices to truly optimize your personal financial strategy?

Risks, trade-offs, and blind spots

While the digital transformation of finance offers unprecedented convenience and innovation, it's equally important to acknowledge the inherent risks, trade-offs, and potential blind spots. Navigating this new financial terrain requires vigilance and an awareness of the challenges that can arise.

Security and Fraud: While financial institutions, both traditional and digital, invest heavily in cybersecurity, digital platforms are constantly targeted by sophisticated fraudsters. Users must remain vigilant against phishing scams, malware, and identity theft. The convenience of digital access also comes with the responsibility of securing your devices and maintaining strong, unique passwords. A trade-off often exists between ease of access and robust security measures, with designers constantly striving for a delicate balance.

Data Privacy: Fintech apps, in particular, often rely on collecting extensive user data to provide personalized insights and services. While this can be beneficial, it also raises concerns about how this data is stored, used, and shared. Understanding the privacy policies of each service is crucial, but often overlooked by busy consumers. The convenience of seamless integration across accounts can come at the cost of a broader digital footprint.

Interoperability & Fragmentation: The specialized nature of many fintech apps means that users often juggle multiple applications for different financial tasks. This fragmentation can lead to a disjointed financial overview, requiring manual aggregation of data or reliance on third-party aggregators. The lack of seamless interoperability between different services can create friction and reduce overall efficiency, negating some of the digital advantages.

Digital Divide: Despite widespread smartphone adoption, a significant portion of the population may still lack access to reliable internet, suitable devices, or the digital literacy required to comfortably use digital-only financial services. This creates a digital divide, potentially excluding vulnerable populations from benefiting from these innovations and further entrenching financial inequality.

Customer Support Limitations: While digital customer support (chatbots, email, phone lines) is often available 24/7, it can lack the personal touch or immediate problem-solving capability of an in-person interaction at a traditional bank branch. For complex issues, language barriers, or during high-stress situations, the absence of human connection can be a significant drawback. As our financial lives become increasingly digital, what unexpected vulnerabilities or complexities might emerge?

Regulatory Ambiguity: The rapid pace of fintech innovation can sometimes outpace regulatory frameworks, leading to areas of ambiguity in consumer protection or accountability. While regulators are actively working to catch up, new services or business models may operate in a grey area, leaving consumers with less clear recourse in case of disputes or failures.

Main points

The modern financial landscape, shaped by digital banking and fintech apps, offers a dynamic array of choices for consumers. Understanding their core differences is key to making informed decisions:

- Distinct Models: Traditional, digital banking, and fintech apps each represent unique approaches to financial services, varying in structure, regulation, and offerings.

- Digital Banks as Full-Service: Digital banks provide comprehensive online banking, excelling in convenience, low fees, and innovative tech, often with deposit insurance via full licenses or partnerships.

- Fintech Apps Specialize: Fintech applications offer niche financial solutions, such as budgeting or investing, prioritizing user experience for specific tasks but requiring users to manage multiple services.

- Regulation is Key Differentiator: Digital banks usually have full banking licenses, providing robust consumer protection; fintech apps have more varied and often less comprehensive regulatory oversight.

- Consumer Empowerment: The diverse options empower consumers to choose financial tools that best match their personal needs, from those valuing in-person service to those embracing digital-only convenience.

- Hybrid Evolution: The industry is moving towards hybrid models, with traditional banks integrating advanced digital features and fintechs partnering with established institutions for broader reach and trust.

- Awareness of Risks: Users must be vigilant about security, data privacy, and the potential fragmentation that comes with managing multiple digital financial platforms.

As the digital financial revolution continues, informed choices are more crucial than ever. Empower yourself by understanding these distinctions, and choose the financial tools that best navigate you through the evolving digital frontier.