The Invisible Connectors: Unpacking the Power of Fintech API Integration

Driving Innovation and Seamless Experiences Across Modern Financial Services

Have you ever wondered how your budgeting app instantly pulls data from your bank, or how a single tap completes a complex payment across different platforms? The secret lies in a silent revolution: Fintech API Integration.

Modern finance demands instant, secure, and personalized services. The ability for different systems to 'talk' to each other isn't just a convenience; it's the engine. What enables this crucial interconnectedness?

Financial technology innovates relentlessly, with new solutions emerging daily. But how do these groundbreaking tools avoid isolated silos, instead forming a powerful, cohesive ecosystem?

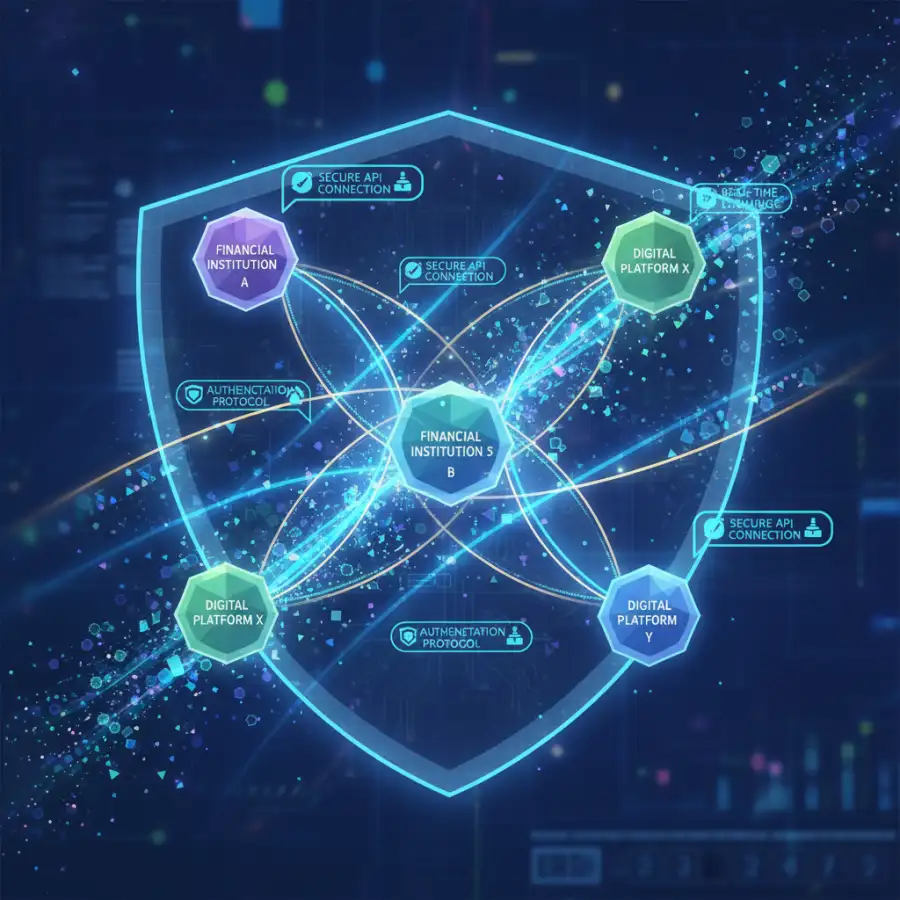

In the digital age, our financial lives are increasingly interconnected, dynamic, and reliant on technology. From instant payments and personalized budgeting tools to sophisticated investment platforms, the modern financial experience is defined by seamless digital interactions. Behind this apparent simplicity lies a complex and powerful technological force: Fintech API Integration. An Application Programming Interface (API) acts as a digital messenger, allowing different software applications to communicate and exchange data securely and efficiently. In the context of financial technology, these APIs enable everything from a banking app sharing transaction data with a personal finance manager to a payment gateway processing a credit card payment on an e-commerce site.

This integration is not merely a technical detail; it's the backbone of innovation, fostering collaboration between traditional financial institutions and nimble fintech startups. It breaks down monolithic systems, enables new possibilities for personalization, and drives the rapid pace of change we observe in "fintech news today." Without robust API integration, the innovative services we now take for granted would operate in isolated silos, unable to utilize the vast potential of combined data and functionality. This guide demystifies Fintech API Integration, exploring its fundamental concepts, transformative power, real-world applications, underlying technologies, and profound impact on both businesses and consumers as we navigate an interconnected financial future.

Quick navigation

- The Invisible Architecture: What Exactly is Fintech API Integration?

- The Transformative Power: Why Fintech APIs Are Essential for Modern Finance

- Real-World Applications: Fintech API Integration in Action

- Key Technologies and Standards Driving API Innovation

- Staying Ahead: The Pulse of Fintech News Today

- What this means for you

- Risks, trade-offs, and blind spots

- Main points

The Invisible Architecture: What Exactly is Fintech API Integration?

To truly grasp the significance of Fintech API Integration, we must first understand what an API is. At its simplest, an API (Application Programming Interface) is a set of rules and protocols that allows different software applications to communicate with each other. Think of it as a waiter in a restaurant: you (the user) tell the waiter (the API) what you want (a request), the waiter goes to the kitchen (the server or another application), retrieves your order, and brings it back to you. You don't need to know how the kitchen prepares the food; you just need the waiter to deliver it correctly.

In the financial world, Fintech API Integration refers to the process of seamlessly connecting disparate financial systems, services, and applications using these digital messengers. This can involve connecting a bank's core system with a mobile banking app, enabling a third-party budgeting tool to access transaction data, or allowing an e-commerce platform to process payments through various providers. The magic happens behind the scenes, where APIs act as secure digital bridges, translating requests and responses between different software programs.

This concept is particularly central to the rise of "Open Banking," a regulatory initiative in many parts of the world that mandates banks to open up their data (with customer consent) to third-party providers via APIs. This allows for a much richer ecosystem of financial services, moving away from a siloed model towards one where data and functionality can be shared to create more innovative products. By providing standardized, secure pathways for information exchange, Fintech API Integration makes it possible for new services to be built quickly, existing ones to be enhanced, and for users to have a more unified and powerful financial experience. How do seemingly disparate financial tools effortlessly 'speak' to each other, creating a unified experience?

The Transformative Power: Why Fintech APIs Are Essential for Modern Finance

The rise of Fintech API Integration isn't just about technical convenience; it's a fundamental shift in how financial services are delivered and consumed. Its transformative power stems from several key areas that are reshaping the modern financial landscape:

- Accelerated Innovation: APIs allow developers to build new financial products and features much faster. Instead of creating every component from scratch, they can utilize existing services via APIs. This plug-and-play approach significantly reduces development time and costs, enabling rapid prototyping and quick market deployment for both startups and established institutions.

- Enhanced Personalization: By securely accessing and integrating customer data (with explicit consent), fintechs and banks can offer highly personalized products and advice. Imagine a loan offer tailored precisely to your spending habits and income, or an investment portfolio dynamically adjusting to your real-time financial goals.

- Seamless Customer Experience: APIs are the silent enablers of the smooth, integrated experiences we now expect. From instantly checking your balance across multiple accounts on a single dashboard to making payments with a single click, APIs reduce friction and improve usability, fostering greater customer satisfaction and loyalty.

- New Business Models (Embedded Finance): Fintech APIs facilitate embedded finance, where financial services are integrated directly into non-financial platforms. Think of buying a car and getting instant loan approval directly from the dealership's website, or a payroll software offering immediate salary advances. This blurs the lines between industries and creates new revenue streams.

- Increased Efficiency & Cost Reduction: Automating data exchange and processes through APIs reduces manual effort, minimizes errors, and streamlines operations. This translates into lower operational costs for financial institutions, potentially leading to more competitive pricing and better services for consumers.

- Strategic Partnerships: APIs foster collaboration. Traditional banks can partner with innovative fintechs to offer advanced services without building them in-house, while fintechs gain access to a bank's established infrastructure and customer base. This synergy drives a richer, more diverse ecosystem.

In essence, APIs act as digital unbundlers and re-bundlers, breaking down traditional financial monoliths into modular services that can be reassembled in novel and powerful ways. This flexibility is what makes these digital bridges so indispensable to the rapid evolution of financial services. What makes these digital bridges so indispensable to the rapid evolution of financial services?

Real-World Applications: Fintech API Integration in Action

The abstract concept of Fintech API Integration truly comes to life when we examine its practical applications, which touch almost every aspect of our modern financial lives. From everyday transactions to complex financial planning, APIs are the invisible threads weaving together a vast web of services.

- Personal Finance and Budgeting Apps: This is one of the most common examples. Apps like Mint, YNAB, or Credit Karma utilize APIs to securely connect to your various bank accounts, credit cards, and investment portfolios. They aggregate your financial data, categorize spending, track net worth, and provide personalized insights, all thanks to the ability of APIs to pull and update information from different sources in real-time.

- Payment Gateways and E-commerce: Every time you make an online purchase, Fintech APIs are hard at work. Payment gateways like Stripe, PayPal, or Square integrate with e-commerce platforms (Shopify, WooCommerce) via APIs. These APIs securely transmit your payment details to the relevant bank or card network, process the transaction, and send back a confirmation, often in mere milliseconds. This enables businesses to accept diverse payment methods without building complex payment infrastructure themselves.

- Lending Platforms: Modern lending platforms, from consumer loans to small business financing, heavily rely on APIs. They integrate with credit bureaus to pull credit scores, connect to bank accounts for income verification, and even link with accounting software for business financial data. This allows for faster, more accurate risk assessment and personalized loan offers, streamlining a process that was once notoriously slow and paper-intensive.

- Fraud Detection and Security: APIs play a critical role in combating financial crime. By integrating with specialized fraud detection services, banks and fintechs can analyze transaction patterns, identify anomalies, and flag suspicious activities in real-time. This quick data exchange across systems is vital for preventing unauthorized transactions and protecting customer funds.

- Wealth Management and Robo-Advisors: Investment platforms and robo-advisors use APIs to access market data (stock prices, economic indicators), integrate with brokerage accounts to execute trades, and connect to client bank accounts for deposits and withdrawals. This automation allows for personalized portfolio management, rebalancing, and tax-loss harvesting with minimal human intervention.

These scenarios show how APIs don't just enable key fintech trends; they are fundamental to many modern financial services. They empower streamlined digital operations for businesses and remarkable convenience for consumers. How do these invisible connections translate into tangible benefits you experience every day?

Key Technologies and Standards Driving API Innovation

Fintech API Integration's effectiveness and security depend on underlying technologies and industry standards that govern digital interactions. Understanding these foundational elements clarifies the robustness and future potential of the interconnected financial ecosystem.

- RESTful APIs and JSON: The vast majority of modern web APIs, including those in fintech, are built on REST (Representational State Transfer) architecture. RESTful APIs are stateless, flexible, and use standard HTTP methods (GET, POST, PUT, DELETE) to interact with resources. Data is typically exchanged using JSON (JavaScript Object Notation), a lightweight, human-readable format that makes it easy for different systems to parse and understand the information being transmitted.

- Security Protocols (OAuth, OpenID Connect): Given the sensitive nature of financial data, robust security is paramount. OAuth (Open Authorization) is a critical standard that allows users to grant third-party applications limited access to their resources (like bank account data) without sharing their actual login credentials. OpenID Connect (OIDC) builds on OAuth to provide identity verification. These protocols ensure that data exchange is authenticated, authorized, and protected from unauthorized access.

- Cloud Infrastructure: The scalability, flexibility, and global reach of cloud computing (AWS, Azure, Google Cloud) are indispensable for modern API integration. Cloud platforms provide the infrastructure to host APIs, manage traffic, ensure high availability, and store data securely. This allows fintechs and banks to scale their API-driven services rapidly without massive upfront hardware investments.

- Microservices Architecture: Many modern financial applications are built using a microservices architecture, where an application is broken down into smaller, independent services, each communicating via APIs. This approach allows for greater agility, easier maintenance, and the ability to update or scale individual components without affecting the entire system, perfectly complementing API integration.

- Data Aggregation Technologies: Technologies that allow secure scraping or direct API access to collect data from various financial institutions are crucial for many fintech applications. While screen scraping has historically been used, the move towards Open Banking APIs is creating more standardized, secure, and permission-based methods for data aggregation.

These technologies and standards collectively form the robust infrastructure that underpins the intricate web of Fintech API Integration. They ensure that data flows securely, efficiently, and reliably between diverse platforms, enabling innovation while maintaining the integrity of financial systems. What are the underlying technological gears that keep this complex, interconnected financial machinery running smoothly and securely?

Staying Ahead: The Pulse of Fintech News Today

The world of financial technology is notoriously fast-paced. What's innovative one day can be standard practice the next, and staying informed about "fintech news today" is essential for anyone operating within or benefiting from this sector. Fintech API Integration is not a static concept; it's constantly evolving, driven by new technological breakthroughs, shifting consumer demands, and evolving regulatory landscapes.

Currently, several areas are seeing significant API-driven innovation:

- Artificial Intelligence and Machine Learning: APIs are crucial for integrating AI and ML models into financial services. This enables everything from sophisticated fraud detection algorithms that learn new patterns to AI-powered chatbots for customer service and personalized financial advice. APIs allow these intelligent systems to access and process vast datasets from various sources.

- Blockchain and Distributed Ledger Technology (DLT): While still in early stages for widespread adoption, APIs are bridging traditional financial systems with blockchain networks. This could transform cross-border payments, asset tokenization, and supply chain finance by offering greater transparency and efficiency.

- Embedded Finance Everywhere: The trend of embedding financial services directly into non-financial applications continues to accelerate. APIs facilitate this by allowing businesses in retail, healthcare, and other sectors to offer payments, lending, or insurance products seamlessly within their own customer journeys.

- Sustainability and ESG Fintech: A growing area involves APIs that integrate environmental, social, and governance (ESG) data into financial platforms. This allows for impact investing, green banking products, and tools that help consumers and businesses track their sustainable financial choices.

- Enhanced Security and Biometrics: With continuous threats, APIs are being used to integrate advanced security features like biometric authentication (fingerprint, facial recognition) and behavioral analytics into financial apps, enhancing protection without compromising user experience.

The dynamic nature of fintech means that new APIs, standards, and integration patterns are constantly emerging. For businesses, keeping a finger on the pulse of these developments is key to maintaining a competitive edge. For consumers, understanding these trends helps in choosing the most innovative, secure, and user-friendly financial tools. With innovation moving at lightning speed, how can businesses and consumers remain informed and adaptive to the next wave of financial transformation?

What this means for you

Fintech API Integration, though a largely technical concept, has tangible and profound implications for individuals and businesses alike, fundamentally reshaping how we interact with our money and operate in the financial world. Understanding these impacts can empower you to make more informed decisions and utilize the full potential of modern financial services.

For Consumers: For the individual, API integration translates directly into a more convenient, personalized, and efficient financial life. You benefit from: more choice in financial products and providers, the ability to manage all your accounts from a single dashboard, faster transactions, and highly personalized insights that help you budget, save, and invest smarter. It means less manual data entry, fewer fragmented experiences, and often, more competitive pricing thanks to increased competition. From setting up recurring payments with ease to receiving real-time alerts about your spending, APIs are the unseen force making your digital financial journey smoother and more intuitive. For a comprehensive FinTech understanding, recognizing this impact is vital.

For Businesses (Banks & Fintechs): For financial institutions, both established and emerging, API integration is an engine of growth and operational excellence. It allows traditional banks to modernize their offerings, integrate with innovative fintech solutions, and remain competitive without having to rebuild their entire legacy infrastructure. Fintech startups, in turn, can launch specialized services rapidly, utilizing bank APIs for core functionalities like account creation or transaction processing. This collaborative ecosystem fosters: reduced development costs, faster time-to-market for new products, expanded product offerings, new revenue streams (e.g., through API monetization), and ultimately, a stronger competitive edge in a dynamic market.

Ultimately, Fintech API Integration is about enabling a future where financial services are more accessible, adaptable, and aligned with individual needs, blurring the lines between different providers and creating a truly interconnected global financial system. Beyond convenience, how does this interconnected financial ecosystem fundamentally reshape your everyday economic reality?

Risks, trade-offs, and blind spots

While Fintech API Integration is a powerful catalyst for innovation, it is not without its complexities, risks, and trade-offs. As financial services become increasingly interconnected, new vulnerabilities and challenges inevitably emerge that demand careful consideration from both developers and users.

- Security Risks: The very nature of API integration involves opening up data pathways between systems. While robust security protocols like OAuth are in place, every integration point represents a potential vulnerability. Data breaches, unauthorized access due to weak API security, or phishing attempts targeting API credentials remain significant threats. Ensuring end-to-end security, including rigorous authentication, authorization, and encryption, is a continuous and complex challenge.

- Regulatory Challenges: The rapid pace of fintech innovation often outstrips the evolution of regulatory frameworks. A patchwork of regulations across different jurisdictions can create compliance burdens for businesses. Issues like data residency, consent management for data sharing, and liability in case of service failures become intricate legal and operational puzzles. This ambiguity can slow down innovation or create uncertainty for consumers.

- Data Privacy Concerns: While consumers consent to data sharing, the extent of data collected, how it's used, and with whom it's shared can raise significant privacy concerns. Transparent data policies and robust consent mechanisms are essential, but often challenging to communicate clearly to users. The trade-off between personalized, convenient services and the desire for absolute data privacy is a constant tension.

- Integration Complexity and Maintenance: Managing a multitude of APIs from different providers can become an engineering nightmare. Ensuring seamless compatibility, handling version updates, and maintaining stable connections requires significant technical expertise and resources. A failure in one API can cascade and impact multiple dependent services, leading to outages or disruptions.

- Vendor Lock-in: Relying heavily on specific API providers can lead to vendor lock-in, making it difficult and costly to switch to alternative services if terms change or performance declines. This reduces flexibility and can stifle competition if one provider becomes dominant.

- Scalability Issues: While APIs are designed for scalability, poorly implemented APIs or sudden surges in traffic can lead to performance bottlenecks. Ensuring that integrated systems can handle peak loads without degrading service is a constant optimization challenge.

As we embrace this digital interconnectedness, what are the hidden pitfalls and critical vulnerabilities we must diligently address?

Main points

Fintech API Integration is a pivotal force in modern financial services, driving unprecedented levels of connectivity and innovation. Our exploration reveals several key takeaways:

- APIs as Connectors: Fintech APIs act as secure digital bridges, enabling seamless communication and data exchange between diverse financial applications and systems.

- Innovation Catalyst: This integration fuels rapid innovation, allowing for the quick development of new products, enhanced personalization, and the emergence of new business models like embedded finance.

- Ubiquitous Applications: From personal finance apps and payment gateways to sophisticated lending and wealth management platforms, APIs are fundamental to the functionality of countless everyday financial services.

- Technological Foundations: Core technologies like RESTful APIs, JSON for data exchange, and robust security protocols (OAuth) ensure the secure and efficient operation of these interconnected systems.

- Benefits for All: Consumers gain from increased choice, personalized experiences, and greater convenience, while businesses achieve improved agility, reduced costs, and expanded market reach.

- Challenges Remain: Significant risks persist around security vulnerabilities, regulatory compliance, data privacy, and the complexities of managing numerous integrations.

- Dynamic Evolution: The fintech landscape, driven by API innovation, is constantly evolving, with new trends like AI in finance and blockchain integration shaping its future.

The journey towards a fully integrated and optimized financial ecosystem is continuous. Embracing these advancements responsibly, with a keen awareness of both their potential and their pitfalls, is essential for businesses and individuals alike to thrive in this interconnected future. Stay informed, engage securely, and utilize the power of these invisible connectors to shape your financial world.